Abstract

This paper has as objective to model the key determinants of bank lending in Cameroon using time series data collected mainly from the World Bank database for the period spanning from 1979 to 2019. After exploring related theoretical and empirical literature, Engle and Granger two steps cointegration testing procedure was employed together with the necessary pretesting (unit root tests) and post estimation testing. Results of stationarity tests indicate that variable were a mixture of stationary and first difference. The lagged residual term possess unit root at level indicating that the variables are actually cointegarted and that ECM is relevant. The estimated cointegration regression model and the corresponding ECM were globally significant at one percent and the models were equally adequate with explanatory power of over 73 and 52 percent respectively. The results of the two models revealed that the effect of economic growth on bank lending was positive and highly significant, the effect of interest rate is negative and equally significant, then the effect of Gross Investment rate was also positive but not very significant in the short run. Based on the major findings, bank lending can be encouraged by stimulating the level of economic activities, by reducing interest rate on loans and by encouraging more investment projects.

Keywords

Bank Lending, Cointegration Technique, Cameroon

1. Introduction

The strength of the banking system in every economy is an essential requirement to ensure economy stability and growth

| [25] | Halling M and Hayden, E., (2006) Bank Failure Prediction: A Two-Step Survival Time Approach, Social Economics, Business Journal of Credit Risk. https://doi.org/10.2139/ssrn.904255 . Corpus ID: 3961090. |

[25]

. The financial system can be named as the main pillar of major importance for the stability and the growth of the globalised economy on the whole. Through payment services, intermediation between savers and borrowers and insurance against risk, the well-working economy is ensured. According to Levine (2004)

| [31] | Levine, R., (2004). Finance and Economic growth: Theory and Evidence. NBER Working Paper 10766. |

[31]

financial intermediaries can improve the acquisition of information on firms, intensity with which creditors exert corporate control, provision of risk-reducing arrangements, pooling of capital, and ease of making transactions. This argument favors a well-developed bank-based financial system. McKinnon (1973)

| [36] | McKinnon, R. I. (1973). Money and Capital in Economic Development. Washington DC: Brookings Institution. |

[36]

also suggests that a better functioning bank credit system can alleviate the external financing constraints that impede credit expansion and the expansion of firms and industries.

The financial sector in Cameroon is seasoned with many commercial banks but it is doubtful if they are sufficient in number and developed enough to mobilize adequate deposits needed for the development of the entire nation. It is evidence from literature that for any economy to fully achieve sustainable growth, it must call for the need to increase domestic resource mobilization through well-developed banking institutions that are capable of intermediating sufficient financial resources by bringing large number of savers and borrowers into contact. Economic growth and development are among the major objectives of the Government and one of the most recommended ways of achieving it according to McKinnon (1973)

| [36] | McKinnon, R. I. (1973). Money and Capital in Economic Development. Washington DC: Brookings Institution. |

[36]

is to raise the level of commercial bank lending and speed up the rate of resource mobilization in the economy.

The Cameroonian banking industry has continued to grow both in terms of new local and foreign entrants, customer and deposit base, regionalization and increase scrutiny from the regulators specifically the Bank of Central Africa States (BEAC). This new shift in Cameroonian banking industry can be attributed to the liberation of the sector, increased adoption of information technology and improved business environment due to reforms being undertaken in the political, economic, social and cultural fields

| [27] | IMF. (2016). International Financial Statistics. Washington D. C. |

[27]

. With these changes, the level of competition in the banking industry has reached an all level high and coupled with an enlightened customers and increased scrutiny from the regulators, local banks have had to introduce effective bank lending policies. Adoption of such practices have been found to be a source of sustainability more so in such environment characterized by stiff competition and enlightened customers

| [41] | Pham, T. H, (2015), Determinants of Bank Lending, Université de Nantes working paper, pp. 1-28. hal-01158241. |

[41]

. Competitiveness of an organization will lead to sustainability which refers to the development that meets the needs of the present generation without compromising the ability of the future generation to meet their needs

| [14] | Bundland Commission, (1887), world commission on environment and development- WCED. |

[14]

.

The rapid expansion of economic activities, population growth and the advent of recurrent socio-political issues require a steady and more efficient financial sector to finance the growing volume of the happenings. According to BEAC (2021), the volume of outstanding loans granted by the 15 banks operating in Cameroon was 3956.3 billion FCFA which represent barely 18.343 percent of the gross domestic product (GDP) of the country stood at 21569.02 billion Fcfa. Theses bank loans are generated from bank deposits of varied types which include among other the Demand deposits, Savings account deposits, Time deposits.

Bank lending constitutes one of the several forms of financial assets in which the public may keep their wealth. Bank lending forms the base of financial intermediation, without deposits, banks have nothing to lend or invest except the small amount of its initial capital and therefore cannot function

| [32] | Louhichi, A and Boujelbene, Y, (2017), ‘Bank capital, lending and financing behaviour of dual banking systems’, Journal of Multinational Financial Management, vol. 41, pp. 61-79. |

[32]

. The role of bank lending in the growth of commercial banks and other institutions deserves a particular attention. In spite of the paramount role of bank lending to the likelihood of banks, no thorough research has been conducted in Cameroon banking sector to redress the situation. The scanty nature of empirical research in this domain is what has motivated the researcher explore this gap by posing the question as: what are the major determinants of banking lending in Cameroon. From this main research question, proceed the following specific questions:

(1) Does income level have an effect on bank lending in Cameroon?

(2) What is the effect of interest rate on bank lending in Cameroon?

(3) How is investment levels correlate with bank lending in Cameroon?

Having finished with the introduction, the rest of the sections are structured as follows; Section two discusses the theoretical and empirical literature review. Section three centers on research methodology which elaborates on research design, data collection, data analysis techniques and limitation. The fourth section is reserved for the results and discussion. And the fifth section draws the paper into logical conclusion and making possible recommendations.

2. Literature Review

2.1. Theoretical Literature

Among some of the early studies on bank lending, Bernanke and Blinder (1988)

| [10] | Bernanke, B., and Blinder, A. S, (1988). “Credit, money, and aggregate demand”, American Economic Review, 78(2), pp. 435-39. |

[10]

used IS-LM framework in a seminal work to analytically show that monetary policy could have a direct impact on bank lending. Defining domestic money supply as broad money M

3 as a percentage of GDP, which is considered as a proxy for the overall monetary policy, the concluded that lower money supply leads to less domestic credit growth. Ehrmann et al (2003)

| [22] | Ehrmann M., Gambacorta L., Martinez P. J., Sevestre P. and Worms A. (2003), "Financial Systems and the Role of Banks in Monetary Policy Transmission in the Euro Area” In Angeloni I., Kashyap A. and Mojon B., Monetary Policy Transmission in the Euro Area, Cambridge, Cambridge University Press. |

[22]

found that monetary tightening has a severe negative impact on rather undercapitalized banks’ lending. Thus, one can conceive that, the precise relationship between bank capital and lending is mixed. Buccheit (2002)

| [13] | Buccheit L. C., (2002), Sovereign Bonds and the Collective Will [article], Emory Law Journal, Vol. 51, Issue 4, pp. 1317-1364. |

[13]

conducted a study on Syndicated loans and reported that when commercial banks jointly give out loans to a borrower, they are able to efficiently minimize their cost and manage time. Adeola (2020)

| [3] | Adeola Y. O. (2020), Determinants of Bank Lending in Nigeria. Global Journal of Emerging Market Economies 12(3) 378–398. |

[3]

believed that commercial banks will not hesitate to give out loans if they can effectively deal with the problem of asymmetric information through constant surveillance and are able to mitigate lending risks.

Cole (1998)

| [17] | Cole, R. A. (1998). The importance of relationships to the availability of credit. Journal of Banking & Finance, 22(6), 959-977. |

[17]

found out that commercial banks, unlike other lending institutions are very unwilling to give out loans. The reason is because during the period of the 1990s these lenders were pressurized by their regulators to make underwriting benchmark or requirement difficult to attain or meet up with. He further stressed that these banks would consider making credit available to firms with whom they have had a close relationship no matter how long. Chodechai (2004)

| [16] | Chodechai, S. (2004). Determinants of bank lending in Thailand. An empirical examination for the years 1992-1996. Unpublished Thesis. |

[16]

examined the determinants of bank lending in Thailand and his results supported Cole’s second view about past relationships as a criterion in banks’ lending decision. He discovered that when banks have such relationships with borrowers, they are more confident in accessing the borrowers’ privacy concerning their occupations and their financial state at every point in time.

The existing literature on banking indicates that banks’ lending decisions are influenced by both demand and supply factors which can broadly be classified into four categories; bank-specific, macroeconomic, monetary and other factors

| [2] | Adedoyin, and Sobodun, (1996), Commercial Banks Lending Activities in Nigeria, Nigerian Financial Review, 9(3), 36–37. |

[2]

. Bank-specific features include profitability, liquidity and solvency

| [39] | Olokoyo, F. O. (2011). Determinants of commercial banks’ lending behavior in Nigeria. International Journal of Financial Research, 2(2), 61. |

[39]

, and legal and regulatory frameworks comprising creditor rights, collateral and bankruptcy laws, accounting standards and so on

| [1] | Achamoh V. N. and Ngouhouo I., (2016) Does Financial Liberalization and Investment Rate Affect Financial Development in Cameroon? International Journal of Economics and Finance; Vol. 8, No. 2; ISSN 1916-971X E-ISSN 1916-9728. |

| [10] | Bernanke, B., and Blinder, A. S, (1988). “Credit, money, and aggregate demand”, American Economic Review, 78(2), pp. 435-39. |

| [18] | Cottarelli, C., Dell’Ariccia, G., and Vladkova-Hollar, I., (2003), “Early Birds, Late Risers, and Sleeping Beauties: Bank Credit Growth to the Private Sector in Central and Eastern Europe and the Balkans”, IMF Working Paper No. 03/213. |

| [43] | Sharma P. and Gounder, N. (2012) determinants of credit in small open economies: the case of six pacific island countries.: Development Economics: macroeconomic issue in developing countries’ economies Journal. https://doi.org/10.2139/SSRN.2187772 |

[1, 10, 18, 43]

. Monetary variables take into account the monetary policy indicator rate, financing costs and broad money and Macroeconomic variables include economic growth and inflation, while other factors include corruption and bank ownership type

| [41] | Pham, T. H, (2015), Determinants of Bank Lending, Université de Nantes working paper, pp. 1-28. hal-01158241. |

[41]

.

Kosak et al. (2015)

| [29] | Kosak, M, Li, S, Loncarski, I and Marinc, M, (2015), ‘Quality of bank capital and bank lending behaviour during the global financial crisis’, International Review of Financial Analysis, vol. 37, pp. 163-83. |

[29]

and Ivanovic (2016)

| [28] | Ivanovic M. (2016), Determinants of Credit Growth: The Case of Montenegro. Economics Journal of Central Banking Theory and Practice. https://doi.org/10.1515/jcbtp-2016-0013 . Corpus ID: 55188488. |

[28]

also provided evidence that deposit growth contributed positively to lending in Montenegro during pre- and post- crisis periods. conclude that a high proportion of customer deposits have a positive and significant influence on credit growth. These results support the classical loanable funds theory, which states that bank loans depend on pre-existing savings

| [41] | Pham, T. H, (2015), Determinants of Bank Lending, Université de Nantes working paper, pp. 1-28. hal-01158241. |

[41]

. Bank interest rate spread has also been shown to affect lending behaviour. Monetary policy, through a prime rate (Central Bank’s rate) has a transmission mechanism on interest rates in the financial market

| [12] | Borio, C., Mc Cauley, R., and McGuire, P., (2011). “Global credit and domestic credit booms”, Bank for International Settlements Quarterly Review, 3, pp. 43–57. |

[12]

. Bank lending rates are mostly seen as being rigid for the reason that they do not move in tandem with the markets

| [24] | Gambacorta L, Mistrulli P. E., (2004), “Bank Capital and Lending Behaviour: Empirical Evidence for Italy”, Journal of Financial Intermediation, 13 (4): 436–457. |

[24]

.

According to Berger and Udell (2006)

| [8] | Berger, A. N. and Udell, G. F. (2006) A More Complete Conceptual Framework for SME Finance. Journal of Banking & Finance, 30, 2945-2966. |

[8]

bank size is considered as an important determinant of bank lending decision as large and complex banks tend to lend few loans to small scale firms. Stein (2000)

| [45] | Stein J. C. (2000), “Information Production and Capital Allocation: Decentralized vs. Hierarchical Firms, NBER Working Paper No. 7705. |

[45]

reiterated that small banks have comparative advantages in producing soft information whereas large banks also have comparative advantages in lending based on hard information. On the other hand, when large and complex banks are able, through technical expertise, to process soft information about small scale firms, then there would be positive relationship between bank size and lending.

The macroeconomic environment within which a bank operates matter for its lending decision. In the period of economic boom, businesses demand for loans to take advantage of expansion and banks investment opportunities equally soar and in periods of economic recession, demand for credit drops. This provides a pro-cyclical relationship between economic growth and bank lending

| [34] | Malede, M. (2014). Determinants of Commercial Banks’ Lending: Evidence from Ethiopian Commercial Banks. European Journal of Business and Management, ISSN, 2222-1905. |

| [35] | Marquez, R, Dell' Ariccia, G (2006), ‘Lending booms and lending standards’, Journal of Finance, vol. 61, no. 5, pp. 2511-46. |

[34, 35]

. Ahiawodzi and Sackey (2013)

| [4] | Ahiawodzi, A. K., and Sackey, F. G. (2013). Determinants of credit rationing to the private sector in Ghana. African Journal of Business Management, 7(38). |

[4]

, added that banks use different strategies to assess their credit and it is vital for them to consider these guiding rules in carrying out their lending activities. In Italy, Vazakidis and Adamopoulos (2009)

| [48] | Vazakidis, A. and Adamopoulos, A. (2009), “Credit Market Development and Economic Growth”, American Journal of Economics and Business Administration, 1(1), pp. 34-40. |

[48]

indicated that economic growth had a positive effect on credit market development. Again, the central bank’s prime rate serves as an indicator to the movement in key economic variables like inflation which in turn affects interest rates. Through the transmission mechanism, an increase in prime rate negatively affects banks’ lending behaviour.

According to Pham (2015)

| [41] | Pham, T. H, (2015), Determinants of Bank Lending, Université de Nantes working paper, pp. 1-28. hal-01158241. |

[41]

, the determinants of bank lending are grouped into four categories; Internal demand factors, External supply factors, Global factors, and Characteristics of the domestic banking system. Pham (2015)

| [41] | Pham, T. H, (2015), Determinants of Bank Lending, Université de Nantes working paper, pp. 1-28. hal-01158241. |

[41]

noted that financial integration level is captured using the Chinn and Ito (2006)

| [15] | Chinn, M. D., and Ito, H., (2006). “What matters for financial development? Capital controls, institutions and interactions”, Journal of Development Economics, 81, pp. 163–92. |

[15]

index of capital account openness (KAOPEN). The tested hypothesis is that higher financial integration level leads to higher inward capital flows, which in turn facilitate a country’s financing. Bank return on equity (ROE) and bank return on assets (ROA are the two indicators reflect the benefit of a bank. According to Aisen and Fraken (2010)

| [5] | Aisen, A., Franken, M., (2010). “Bank credit during the 2008 financial crisis: a cross-country comparison”, International Monetary Fund Working Paper, No. 10/47. |

[5]

, a bank with sound profitability will most likely have great access to financing, but it could also indicate that banks have taken riskier positions. Bank concentration is an indicator is constructed by Beck et al. (2000)

| [7] | Beck, T., A. Demirgüç-Kunt, and R. Levine, 92000], “A New Database on Financial Development and Structure,” World Bank Economic Review, Vol. 14, pp. 597–605. |

[7]

and defined as total assets of the three largest banks as a percentage of total assets of the banking system. Bank non-performing loans to total gross loans measured in term of soundness of banking system, which can strongly influence the growth of domestic credit

| [41] | Pham, T. H, (2015), Determinants of Bank Lending, Université de Nantes working paper, pp. 1-28. hal-01158241. |

[41]

.

According to Achamoh and Ngouhouo (2016)

| [1] | Achamoh V. N. and Ngouhouo I., (2016) Does Financial Liberalization and Investment Rate Affect Financial Development in Cameroon? International Journal of Economics and Finance; Vol. 8, No. 2; ISSN 1916-971X E-ISSN 1916-9728. |

[1]

, financial liberalization which is viewed as a set of operational reforms and policy measures designed to deregulate and transform the financial system and its structure with the view of achieving a liberalized market-oriented system within an appropriate regulatory framework promotes banking lending. The saw view was upheld by the pioneer theoretical analyses which provided a rationale for financial sector liberalization as a means of promoting bank lending and growth were those of

| [36] | McKinnon, R. I. (1973). Money and Capital in Economic Development. Washington DC: Brookings Institution. |

| [44] | Shaw, E. S. (1973). Financial Deepening in Economic Development. New York: Oxford University Press. |

[36, 44]

. Recently, Ivanovic (2016)

| [28] | Ivanovic M. (2016), Determinants of Credit Growth: The Case of Montenegro. Economics Journal of Central Banking Theory and Practice. https://doi.org/10.1515/jcbtp-2016-0013 . Corpus ID: 55188488. |

[28]

shows that GDP growth contributed to robust credit growth in Montenegro in the pre-crisis period, but not in the post crisis period. This can be explained by the fact that although growth resumed after the crisis it remained moderate mainly due to banks’ risk averse approach. Nguyen and Dang (2020)

| [37] | Nguyen, H. D and Dang, V. D, (2020), ‘Bank-specific determinants of loan growth in Vietnam: Evidence from the CAMELS approach’, Journal of Asian Finance, Economics and Business, vol. 7, no 9, pp. 179-89. |

[37]

found the negative impact of credit risk, measured by rising non-performing loans on bank lending.

2.2. Empirical Literature

Empirical studies on bank lending are not new. In 1998, Panagopoulos and Spiliotis

| [40] | Panagopoulos, Y., &Spiliotis, A. (1998). The determinants of commercial banks’ lending behavior: some evidence for Greece. Journal of Post Keynesian Economics, 20 (4), 649-672. |

[40]

carried out a dissertation on the influencing factors of commercial banks’ lending decision in Greece for the period of 1971-1993 using the panel software analysis and regression model. Their findings exhibited that credit money, money wage bill, and loan customer relation had a strong significant impact on commercial banks’ lending behavior in Greece.

Loutskina (2012)

| [33] | Loutskina Z. (2012), the impact of securitization on bank’s credit risktaking behavior, Simon Fraser University. |

[33]

, in her research study on the role of securitization in bank liquidity and funding management she found out that when banks are able to liquidate their loans in order to meet their liquidity needs, they will be more willing to make credit available to borrowers. According to her, since liquid funds and loans are very vital elements of bank assets there is a negative relationship between liquid funds and lending. That is to say, as the former decreases the later increases. Djiogap and Ngomsi (2012)

| [20] | Djiogap, F., and Ngomsi, A. (2012). Determinants of bank long-term lending behavior in the Central African Economy and Monetary Community. |

[20]

studies the determinants of bank long-term lending behavior in the Central African Economic and Monetary Community (CEMAC) context. The study aimed to test the common bank-level and macroeconomics determinants of bank long-term loan behavior. The model used is estimated using a sample of six countries from the CEMAC. They found that a bank’s ability to extend long-term business loans depends on its size, capitalization, GDP growth and the availability of longterm liabilities. These results underline the importance of supply side constraints in extending vital long-term credit to firms.

Olokoyo (2011)

| [39] | Olokoyo, F. O. (2011). Determinants of commercial banks’ lending behavior in Nigeria. International Journal of Financial Research, 2(2), 61. |

[39]

, examined banking lending in Nigerian economy for the period of 1980-2005. From her findings, the predictor variables (volume of deposits, investment portfolio, foreign exchange, and GDP) were statistically significant and portrayed a positive relationship with commercial bank lending. This implies that these explanatory variables are very vital for banks’ lending decisions to give out loans and advances to borrowers. She suggested that commercial banks in Nigeria should improve their management skills and lending performance by building up new strategies and system that will pull deposits irrespective of its source.

Malede (2014), examined the determinants of commercial banks’ Lending in Ethiopia over a 6-year period (2005-2011). He applied the panel data analysis and OLS to find out that credit risk, bank size, GDP, liquidity, lending rate and investment were statistically significant and had a positive relationship with commercial banks’ lending. He concluded that these explanatory variables greatly influenced banks’ lending decisions compared to deposit and cash required reserve which was insignificant. He suggested that commercial banks should throw more light on their credit risk and better manage their liquidity ratio because these variables prevent their willingness to lend.

| [47] | Tomak S., (2013). Determinants of Commercial Banks’ Lending behavior: evience from Turkey. Asian Journal of empirical research. Aasian economic and social society, vol. 3(8) pp 933-943. |

[47]

, investigated on bank lending in Turkey starting from the period 2003-2012 considering 18 banks for the sample size. His results showed that GDP and interest rate were statistically insignificant. On the other hand, banks total liabilities, NPL, size and inflation rate were statistically significant and had a positive relationship with commercial banks’ lending behavior.

Pham (2015)

| [41] | Pham, T. H, (2015), Determinants of Bank Lending, Université de Nantes working paper, pp. 1-28. hal-01158241. |

[41]

investigated the determinants of bank credit by using a large data set covering 146 countries at different levels of economic development over the period 1990-2013 using GMM. They find evidence of the country specific effect of economic growth on bank credit. Empirical results also suggest that the health of domestic banking system plays a relevant role in boosting bank lending. By contrast, the dependence on foreign capital inflows of a country can make its domestic banking sector more vulnerable to external shock and then to face credit boom-bust cycles. Ladimel, kumankoma, and Osei (2013)

| [30] | Ladime j, kumankoma E. S., and Osei K., (2013 Determinants of Bank Lending Behaviour in Ghana Jounrnal of economics and sustainable Development Vol 4, No 17 pp. 1-7. |

[30]

investigated the determinants of bank lending behaviour in Ghana. Using the GMM-System estimator developed by Arellano and Bover (1995)

| [6] | Arellano, M., and Bover, O., (1995), “Another Look at the Instrumental Variable Estimation of Errorcomponents Models” Journal of Econometrics, 68, 28–52. |

[6]

and Blundell and Bond (1998)

| [11] | Blundell, R., and Bond, S., (1998). “Initial conditions and Moment Restrictions in Dynamic Panel Data”, Journal of Econometrics, 87, pp. 115-44. |

[11]

, they found that bank size and capital structure have a statistically significant and positive relationship with bank lending behaviour. They also find evidence of negative and significant impact of some macroeconomic indicators (central bank lending rate and exchange rate) on bank lending behavior. Again, competition in the industry was found to have a positive and significant impact on bank lending behaviour. It was remarked from the study that policies aimed at maintaining stable macroeconomic fundamentals would greatly accelerate bank lending decision.

Adeola (2020)

| [3] | Adeola Y. O. (2020), Determinants of Bank Lending in Nigeria. Global Journal of Emerging Market Economies 12(3) 378–398. |

[3]

on his part studied the determinants of bank lending in Nigeria. Use was made of the parsimonious model to investigates the impact of growth in loan-to-deposit ratio, growth in inflation, growth in broad money, and growth in bank capital on growth in bank lending using annual data from 1961 to 2016. This study adopts the autoregressive distributed lag (ARDL) bounds testing approach and Granger causality tests to investigate the relationship and direction of causality among the variables, respectively. The Granger causality tests show that growth in broad money Granger-causes growth in bank lending, while there is no causality from other explanatory variables to bank lending in Nigeria. equally that growth in bank lending Granger-causes growth in loan-to-deposit ratio and growth in inflation in Nigeria.

Ranadi et al (2021)

| [42] | Ranadi K., Hesaie J., Vosamacala S., Kabir M. N., Miah D., and Sharma P. (2021), determinants of bank lending in PICs. Griffith Asia Institute. Reserve bank of Fiji. |

[42]

, examines the determinants of bank lending in three Pacific Island Countries including Fiji, Vanuatu, and the Solomon Islands using data collected from 21 financial institutions comprising of 15 banks and 6 credit institutions for the period of 2000-2018, making a final dataset of 229 firm-year observations. The study make use of ordinary least square (OLS), fixed effect, and system Generalised Method of Moments (GMM) estimation techniques. Results show that banks’ asset size, core capital, customer deposits, and profitability are positively related to loan growth meanwhile interbank deposit and non-performing loans negatively affect banks’ loan growth. The results remain robust when alternative proxy for bank lending were applied.

None of the empirical study on the determinants of bank lending has so far be conducted using recent Cameroon’s time series data. The paucity of this empirical studies has motivated us to fill this gap in research as a challenge.

3. Methodology

3.1. Data Collection and Sources

Empirical investigation in this study makes use of annual time series data spanning from 1979 to 2020. The data are collected from the World Development Indicators CD-ROM (2021), the International Financial Statistics, IFS, CD-ROM (2020), the National Institute of Statistics (NIS) in Yaounde and the Bank of Central Africa state, BEAC, (2021).

3.2. Analytical Procedure

Specification of the long run model of bank lending

To empirically investigate the relationships between bank lending and its determining variables, time series data are compiled from varied sources. The following cointegration equation is specified:

Log(BL)t= b0+ b1Log(GDP)t+ b2(IR)t+b3Log(INV)t+ b4Log(OP)t+ b5(INFL)t+ b6(GOV)t+ et(1)

Where;

LogBL is the Log of bank lending taken as Credit to private sector as a % of GDP

Log(GDP) is the log of Level of economic activities proxy as annual % growth of GDP

IR is the Real interest rate

Log(INV) is the log of investment levels taken as ratio of gross investment as a % of GDP

Log(OP) is the log of Openness taken as sum of import and export as a % of GDP

INFL is the Rate of inflation measured as the % change in Consumer Price Index

Log(GOV) is the log of government final consumption expenditure as a % of GDP

et is the error term

3.3. Variables Description

3.3.1. The Dependent Variable

Bank lending (BL)

Bank lending is measured in terms the ratio of credit to the private sector to GDP as used in ThiHong (2015) among others. This indicator recognizes bank lending as financial resources to the firms and individual. It isolates credit issued to the private sector, as opposed to credit issued to public sector or issued by the central bank. Private credit ratio has been extensively used because it improves on other measures of bank lending

| [31] | Levine, R., (2004). Finance and Economic growth: Theory and Evidence. NBER Working Paper 10766. |

[31]

. Higher level of private credit ratio is interpreted as higher level of financing services and therefore greater financial intermediary development.

3.3.2. The Independent Variables

Level of economic activities (GDP)

The expansion of economic activities requires more financial service as different sectors of the economy demand credit for obvious reasons thereby accelerating bank lending. Economic activities level is benchmark measure of the economy health and reflects the demand for credit

| [23] | Frankel, J., and Romer, D., (1999). “Does trade cause growth?”, American Economics Review, 89 (3), pp. 379–399. |

[23]

. Higher domestic income corresponds to stronger domestic demand for credit

| [46] | Takats, E., (2010). Was it credit supply? Cross-border bank lending to emerging market economies during the financial crisis. Bank for International Settlements Quarterly Review, 2, pp. 49– 56. |

[46]

. The growth rate of an economy captured in this study by annual growth rate of real GDP is therefore expected to have a positive effect on bank lending.

Real interest rate (IR)

Increase in interest rates enable households to benefit higher rate of return on their deposits in the bank meanwhile investors lose part of profitable due to increase in cost of capital. Real interest rate is taken in this study as the lending interest rate adjusted for inflation. Increase in real interest rate reduce the profit of investor in funding their project with borrowed funds. Interest is hypothesized to have inverse relationship with bank lending.

The investment levels (INV)

Investment rate is taken as the ratio of gross investment to Gross Domestic Product. Total investment is made up of foreign direct investment and domestic fixed capital formation. As the rate of investment in an economy increases either by foreigners or indigenes, there is high demand for financial services. The volume of investment is related to the efficiency with which financial sector channel credit to the private sector

| [19] | De Gregorio J. and Guidotti, E. P. (1995). Financial development and economic growth. world development vol 23, issue 3. Pp 433-448. |

[19]

. Gross investment rate is expected to contribute positively to the bank lending of a country.

Apart from our three main factors, there are equally other determinants of banking lending which are considered in the ongoing study as controlled variables. The variables include;

3.3.3. Controlled Variables

Openness of the economy (OP)

Trade openness is measured as the sum of total exports and imports divided by GDP of a country. Trade openness may result to higher bank lending even though it may expose a country to be more vulnerable to international shocks such as a dramatic collapse in global trade as it was the case during the period 2008-2009. According to Do and Levchenko (2004)

| [21] | Do, Q. T., and Levchenko, A. A. (2004). Trade and financial development. World Bank Working Paper Series (3347). |

[21]

and Huang and Temple (2005)

| [26] | Huang, Y., & Temple, J. R. W. (2005). Does external trade promote financial development? CEPR discussion paper No. 515. |

[26]

, policies which encourage openness to external trade tend to boost bank lending. Openness variable is expected to have a positive sign.

Rate of inflation (INFL)

The rate of inflation is captured by change in the Consumer Price Index. Inflation leads to arbitrary distribution of income and tend to penalize depositors in favour of borrowers. It makes people to save their financial resources in assets form rather than bank deposits. Persistent increase in general price level equally renders most functions of money ineffective and increases degree of uncertainty. With all these, it is reasonable to expect that inflation adversely influences bank lending both in the short and long run.

The size of the government (GOV)

Size of the government measured by General Government final consumption expenditure may likely influence the rate of bank lending in the country. Government expenditure may have either a positive or negative impact on bank lending, depending on the financing effects of the government.

3.4. Error Correction Model of Bank Lending

To capture short run adjustments of bank lending from longrun model, we specify a flexible dynamic distributed lag model which includes an error correction term from a cointegrating regression as in equation (

2).

∆Log(BL)

t= a +

∆Log(BL)

t= a +

∆Log(GDP)

t-j+

∆Log(IR)

i,t-j+

∆Log(INV)

i,t-j+

∆Log(INFL)

i,t-j+

∆(OP)

i, t- j+

∆(GOV)

i, t-+π

+μ

t(2) where

is the predicted residual term from a co-integrating relationship estimated from the long-run model in equation (

1), π is the coefficient of the error correction term,

∆ is the difference operator and μ

t is the usual white noise. This procedure is however valid only if, at least, a co-integrating relation exists among the variables irrespective of whether there possess unit roots at level form or not. This entails testing for the significance level of the lagged residual term (

) included in the ECM (equation

2). When lagged error term is significant, the variables are said to be cointegrated and error correction terms exist to account for short run deviations from the long run equilibrium relationship implied by the cointegration.

3.5. Estimation Procedure

The method of cointegration is employed in estimating the bank lending equations. This method has gained increasing importance in analyses that describe equilibrium relationships. A necessary condition for integration, however, is that the data series for each variable involved exhibit similar statistical properties. Empirical analysis in this paper is done in two phases. In the first phase, the statistical properties of the variables are verified through the unit roots test and in the second phase, the existing relationship is tested for cointegration.

3.6. Pretesting Procedure

3.6.1. Unit Roots Tests

As a pretesting, Augmented Dickey Fuller (ADF) test and Phillips Perron unit roots testing is conducted to ensure stationarity of the variables before estimation. The essence of conducting two distinct stationarity tests is to ensure that series enter model to be estimated in non-explosive form and mainly to address the issue of tests with low power

| [38] | Okechukwu G. O. & Chukwuma A., 2008. "How Competitive and Efficient are Nigerian Ports?," Palgrave Macmillan Books, in: Paul Collier & Chukwuma C. Soludo & Catherine Pattillo (ed.), Economic Policy Options for a Prosperous Nigeria, chapter 12, pages 275-299, Palgrave Macmillan. |

[38]

. In the two tests, if the null hypothesis is being accepted, it means that the series is not stationary, otherwise, the alternative hypothesis of unit roots is accepted. The next step after testing whether or not the variables are stationary is to test their cointegrating relationship.

3.6.2. Cointegration Test

The main reason for the popularity of co-integration analysis is that it provides a formal background for testing and estimating short-run and long-run relationships among economic variables. Engle and Granger two steps cointegration test is applied in this study. According to this method, testing cointegration between commercial bank lending and its explanatory variables simply requires first, to run an Ordinary Least Squared (OLS) regression and retained the residuals. At the second step, ADF or PP tests is applied on the residual, in order to determine whether or not it is stationary. When the residual term is stationary, it indicates that the two series are cointegrated and that the corresponding ECM can be estimated.

Error correction model is estimated by simply reintroducing the lagged value of residual term of the cointegrating equation as one of the explanatory variables. The other variables from the cointegrating regression enter the ECM as a difference or stationary variables depending on the results of unit roots pretesting of the time series in question. That is, the number of times a variable is difference corresponds to the order of the integration of the series as determine by the ADF and PP unit roots test.

3.7. Post Estimation Testing Procedure

Finally, we apply the Breusch-Godfrey Serial Correlation LM Test for serial correlation of successive error terms, the ARCH (Auto-regressive Conditional Heteroscedasticity) test for heteroscedasticity and the Jarque-Bera test for normality of errors to verify if these regressions are in the correct functional form or not.

4. Presentation and Discussion of Results

4.1. Presentation and Interpretation of Results Findings

The results of pretesting, trend analysis, cointegration analysis and post estimation test on residual are presented in that order.

4.1.1. Descriptive Analysis

Before getting into the data analysis of the study, a prior statistical analysis relative to the sample of study needs be effectuated.

Table 1 below summarizes the descriptive statistics relative to the variables used for the period of study.

Table 1. Summary of Descriptive Statistics of Variables.

| N | Minimum | Maximum | Mean | Std. Deviation |

Bank Lending | 41 | 5.9388 | 31.2423 | 15.646639 | 8.2595683 |

GDP Growth | 41 | -7.8000 | 17.0827 | 3.816054 | 4.1780979 |

Real Interest rate | 41 | 2.4500 | 8.7500 | 5.043690 | 1.8076577 |

Invt Rate | 41 | 14.3054 | 40.6004 | 21.745051 | 3.8639058 |

Degree of Openess | 41 | 13.2264 | 32.5123 | 23.961195 | 4.5832524 |

Inflation Rate | 41 | 19.6707 | 115.8080 | 72.147805 | 30.3240672 |

Govt Exp | 41 | 8.8377 | 14.3968 | 11.210310 | 1.2052507 |

Valid N (listwise) | 41 | | | | |

Source: Author computation using data from WDI (2020)

From the above, the scale of the variables was very large compared to the other variables hence there was the need of logging the variable so as to reduce the scale. Therefore, the variable save was logged before running regression of our study so as to reduce the scale effect of the variable.

4.1.2. Correlation Analysis

Correlation matrix is constructed to have a previewed knowledge of the relationship between the variables. The results of the correlation matrix are presented on

table 2 below.

Table 2. Correlation Matrix.

| Bank Lending | GDP Growth | Real Interest rate | Invt Rate | Degree of Openess | Inflation Rate | Govt Exp |

Bank Lending | 1.000 | | | | | | |

GDP Growth | .138 | 1.000 | | | | | |

Real Interest rate | .414 | -.119 | 1.000 | | | | |

Invt Rate | .085 | .432 | -.182 | 1.000 | | | |

Degree of Openess | .089 | .585 | -.184 | .194 | 1.000 | | |

Inflation Rate | -.663 | -.023 | -.870 | .078 | .029 | 1.000 | |

Govt Exp | -.394 | -.567 | -.198 | -.269 | -.570 | .410 | 1.000 |

Source: Authorcomputation using data from WDI (2020) and SPSS 25

The correlation results presented in Table above, show that there exist both positive and negative relationships between the variables included in the study. This table shows both the relationship between the independent and the dependent variables and between the independent and independent variables. The correlation results could also be used as a prelude to investigate the presence of multicollinearity within the independent variables if the correlation coefficient is as large as 0.7 or more. it implies that there exists a weak correlation between the pair of variables and if the correlation coefficient is more than 0.7, it implies that there exists a strong correlation between the pair of variables.

4.1.3. Results of Augmented Dickey-Fuller (ADF) Unit Roots Test

The table below presents the Augmented Dickey-Fuller (ADF) unit roots test results. This consists of rejecting or accepting the null hypothesis, Ho, of unit roots or non stationarity of the series. The results are presented in the

Table 3.

Results of ADF unit roots test.

The table below presents the Augmented Dickey-Fuller (ADF) unit roots test results. This consists of rejecting or accepting the null hypothesis, Ho, of unit roots or non stationarity of the series. The results are presented in the

Table 3.

Table 3. Results of ADF Unit Roots.

variables | ADF unit root test | Order of integration |

Level Form | First difference |

Log (BL)t | -1.244 | -2.222b | I(1) |

Log (GDP)t | -2.90 a | -4.522 | I(0) |

(IR)t | -2.90 a | -4.522 | I(1) |

Log (INV)t | -2.162 | -5.421 a | I(1) |

Log (OP)t | -1.201 | -4.154 a | I(1) |

(INFL)t | -2.555b | -6.124 | I(0) |

Log (GOV)t | -1.222 | -4.101 a | I(1) |

MacKinnon critical values at 1%, 5% and 10% are respectively -2.6496, -2.9558 and -2.6164. (a), (b) indicate variables significantly stationary at 1% and 5% levels of confidence respectively.

Source: By Author

The results depict that most of the variables used in this study are integrated to the order one, I(1) except the variable for growth rate, rate of inflation, and that of banking crisis.

4.1.4. Result of Cointegration Testing

The results of cointegration regression equation of Bank lending are presented in

Table 2.

Table 4. Results of cointegrating regression of Bank lending in Cameroon.

Dependent Variable: Log of Bank lending- (LogBL)t |

Independent Variables | Coefficient | t-statistics |

Constant | 2.150* | 1.802 |

Levels of economic activities: Log(GDP)t | 0.619*** | 2.844 |

Real interest rate: (IR)t | -0.920** | -2.462 |

Log of investment rate: (LogINV)t | 0.314* | 1.806 |

Log of the degree of openness: (LogOP)t | 0.124* | 1.824 |

Rate of inflation: (INFL)t | -0.259 | -0.841 |

Log of government spending: (LogGOV)t | 0.002 | 0.254 |

Augmented Dickey-Fuller unit root test | -3.216*** |

R-squared | 0.792 |

Adjusted R-squared | 0.731 |

F-statistic | 21.04 (p=0.001) |

Superscript ***, **, * indicate significance at the 1, 5, and 10% levels, respectively.

Source: By Author

The result of unit roots test on residuals is included in

Table 4. The intention of the test was to verify whether longrun relationships exist between the variables or not. The ADF test on the lagged value of the error correction term possesses unit root at level form, indicating that the Error correction model does not exist according to ADF statistics as the calculated value of ADF is greater than its critical value at the 1 percent. This is an indication that longrun relationship exists between the variables. The error terms of both models are negative and stationary at the level form following ADF unit roots tests which signify that the error correction dynamics of the models can be estimated as in

Table 5.

The results of the error correction models reported in

Table 5 suggest that Bank lending in the short run is determined by growth rate of gross domestic product, inflation rate and the first differences of the degree of openness. First difference of gross investment rate bears the expected positive sign in both models but was only significant in the cointegration model.

Table 5. Results of Error Correction Model for Bank Lending in Cameroon.

Dependent Variable: Δ(LogBL) t |

Variables | ECM | t-statistics |

Constant | 0.014 | 0.410 |

Log of the Levels of economic activities: Log(GDP)t | 0.222** | 2.038 |

Change in Real interest rate: Δ(IR)t | -0.050** | -0.0462 |

Change in the Log of investment rate: Δ(LogINV)t | 0.062 | 0.806 |

Change in theLog of the degree of openness: Δ(LogOP)t | 0.259* | 1.731 |

Rate of inflation: (INFL)t | 0.002 | 0.254 |

Change in theLog of government spending: Δ(LogGOV)t | 0.106 | 0.524 |

(ECT)t-1 | -0.5371*** | -2.163 |

R-squared | 0.212 |

Adjusted R-squared | 0.521 |

F-statistic | 4.488 (P= 0.002) |

Superscript ***, **, * indicate significance at the 1, 5, and 10% levels, respectively

Source: By Author

The lagged error-correction terms ‘0.5371’ for the ECM is bearing a correct sign, and the variable is highly significant. This is an indication that about 53 percent of shocks on the Bank lending are corrected by the “feed-back” effect annually according to the results of the Error Correction Model.

4.1.5. Diagnostic and Post Estimation Test on the Residual

Some diagnostic Tests were conducted on the residual of the regression model to ascertain that the model is in the correct functional form. The tests include the test for normality, heteroscedasticity and test for autocorrelation of the residual term.

The results of diagnostic tests on residual applied to the cointegration and error correction models report no evidence of serial correlation of successive error terms nor Heteroscedasticity effect in the error terms as the probability value of for all the tests instead exceed 0.05 implying that there are statistically insignificant at 5% level of significant. (the null hypothesis is not rejected). Furthermore, Ramsey Reset test results show that the cointegration model and corresponding ECM are correctly specified since the probability of the Ramsey is greater 0.05 in both models. The models also pass the Jarque-Bera normality test which suggests that the errors are normally.

Table 6. Results of post estimation test on the residual.

Residual Diagnoses tests | Cointegration model | Error correction model |

Statistics | Probability | Statistics | Probability |

Ramsey Reset | 3.401 | 0.411 | 1.314 | 0.317 |

Jacque- Bera for Residual Normality | 4.330 | 0.131 | 2.818 | 0.306 |

Breusch-Godfrey Serial Correlation LM Test` | 3.471 | 0.149 | 2.104 | 0.316 |

ARCH LM test of heteroscedasticity | - | - | 3.635 | 0.193 |

White Noise heteroscedasticity | 3.609 | 0.348 | - | - |

Source: by author using Eviews 9

4.2. Discussion of Findings

The results of these tests indicate the absence of multicollinearity within the independent variables as pairwise correlation coefficients are weak (less than 0.7). The results of unit roots test conducted using Augmented Dickey-Fuller (ADF) tests depict that all the variables used in this study are integrated to the order one, I(1) except the variable for growth rate, and interest rate. Trend analysis results show great fluctuations in almost all the variables under this study. The unit root test on the error correction term (ECT) is significant at 1 percent and its coefficient bears the correct negative sign, indicating that Bank lending is really cointegrated with its determining factors.

The coefficient estimates for level of GDP growth, interest rate and that of gross investment to GDP ratio in the cointegration regression results presented in

Table 4 and those of the corresponding ECM estimated in

Table 5 report the following empirical relations between these variables and Bank lending in Cameroon.

For the first research hypothesis, it was found that the effect of GDP growth used in capturing level of income in the economy has a highly significant and positive relationship with bank lending in Cameroon. GDP growth was significant at 1 percent in the cointegration regression model and at 5 percent in the short run as in the error correction model. A similar result result was obtained by Vazakidis and Adamopoulos (2009)

| [48] | Vazakidis, A. and Adamopoulos, A. (2009), “Credit Market Development and Economic Growth”, American Journal of Economics and Business Administration, 1(1), pp. 34-40. |

[48]

even though Tomak (2013)

| [47] | Tomak S., (2013). Determinants of Commercial Banks’ Lending behavior: evience from Turkey. Asian Journal of empirical research. Aasian economic and social society, vol. 3(8) pp 933-943. |

[47]

found the relationship to be statistically insignificant in Turkey.

For the second research hypothesis, the result of the cointegration regression indicates that interest rate is another very crucial determinant of bank lending in Cameroon. The variable has a negative and is significant at 5 percent in explaining variations in the Bank lending in the long run as it was hypothesized. From the error correction model used in capturing short run dynamics among variable, the effect of the interest rate was equally significant at 5 percent. This result is however contrary to that of Tomak (2013)

| [47] | Tomak S., (2013). Determinants of Commercial Banks’ Lending behavior: evience from Turkey. Asian Journal of empirical research. Aasian economic and social society, vol. 3(8) pp 933-943. |

[47]

on the study bank lending of 18 banks in Turkey from 2003-2012.

For the third research hypothesis, findings from this study indicates that gross Investment rate taken as gross fixed capital formation as a percentage of GDP was found as a positive correlate of bank lending in both the short run and long run. Investment level was however ever significant only at border line in promoting bank lending in Cameroon in the long run model and the variable was not very significant in the short run. The result is in line with the one obtained over two decades ago by

| [19] | De Gregorio J. and Guidotti, E. P. (1995). Financial development and economic growth. world development vol 23, issue 3. Pp 433-448. |

[19]

.

Openness of the economy captured in term of the average of export and import as percentage of GDP was also reported as a positive correlate of bank lending in both the short run and long run models but instead significant at 10 percent. Variable for Inflation rate and that of government expenditure were not very significant in determining banking lending in Cameroon during the period under study.

The two models reported in

Tables 4 and 5 are globally significant at 1 percent, as indicated by their various F-statistics with respective coefficient of determination of 73.1 percent and 52 percent for cointegration model and the Error correction model.

The results of diagnostic tests applied to the cointegration and error correction models report no evidence of serial correlation of successive error terms nor Heteroscedasticity effect in the error terms. The models also pass the Jarque-Bera normality test which suggests that the errors are normally distributed and Ramsey Reset test which indicates that the model were specified correctly. Meaning that these results are consistent and confirm by the post- test estimations, which confirm that, the model does not suffer from any econometrics problems. Hence, the results can be used for policy recommendation.

5. Conclusion

The intention of this study was to model the key determinants of bank lending in Cameroon. To attain this objective, both theoretical and empirical literature sources were explored and times series data were collected to verify the three hypotheses of the study. Use was made of cointegration testing procedure while respecting all the necessary pretesting and post estimation testing, the result of the study permits us to conclude that all the hypotheses were attained event though the third hypothesis was not achieved satisfactorily.

The effect of economic growth rate was positive as hypothsized (H1) and highly significant in influencing bank lending in Cameroon. The effect of interest rate on bank lending was negative as anticipated (H2) and it is equally significant in accounting for changes on bank lending in Cameroon. Gross Investment rate is found as another positive correlates of bank lending in both the short run and longrun as hypothesized (H3) but not very significant especially in the shortrun.

6. Recommendations

Based on the major findings highlighted, Bank managers together with the board of directors and policy makers could encourage bank lending by increasingly design policies that would stimulate the level of economic activities.

Stakeholders of banks can equally foster the bank lending by lowering interest on loans so as to make borrowed funds more attractive to investors.

Encouraging investment projects can as well increase the demand for bank credit and therefore help to step-up the level of bank lending in the economy

Author Contributions

Achamoh Victalice Ngimanang is the sole author. The author read and approved the final manuscript.

Conflicts of Interest

The authors declare no conflicts of interest.

Appendix

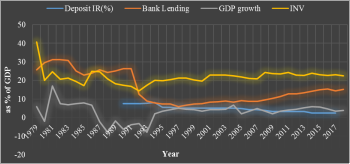

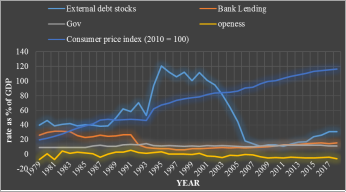

Trends of variables 1979-2018

Dependent Variable And Main Independent Variables

Figure 1. Evolution of deposit interest rate, Bank lending, GDP growth and Investment rate in Cameroon from 1979 to 2019.

Dependent Variable and Controlled Variables

Figure 2. Evolution Bank lending, government expenditure, openness, inflation rate external debt in Cameroon from 1979 to 2019.

References

| [1] |

Achamoh V. N. and Ngouhouo I., (2016) Does Financial Liberalization and Investment Rate Affect Financial Development in Cameroon? International Journal of Economics and Finance; Vol. 8, No. 2; ISSN 1916-971X E-ISSN 1916-9728.

|

| [2] |

Adedoyin, and Sobodun, (1996), Commercial Banks Lending Activities in Nigeria, Nigerian Financial Review, 9(3), 36–37.

|

| [3] |

Adeola Y. O. (2020), Determinants of Bank Lending in Nigeria. Global Journal of Emerging Market Economies 12(3) 378–398.

|

| [4] |

Ahiawodzi, A. K., and Sackey, F. G. (2013). Determinants of credit rationing to the private sector in Ghana. African Journal of Business Management, 7(38).

|

| [5] |

Aisen, A., Franken, M., (2010). “Bank credit during the 2008 financial crisis: a cross-country comparison”, International Monetary Fund Working Paper, No. 10/47.

|

| [6] |

Arellano, M., and Bover, O., (1995), “Another Look at the Instrumental Variable Estimation of Errorcomponents Models” Journal of Econometrics, 68, 28–52.

|

| [7] |

Beck, T., A. Demirgüç-Kunt, and R. Levine, 92000], “A New Database on Financial Development and Structure,” World Bank Economic Review, Vol. 14, pp. 597–605.

|

| [8] |

Berger, A. N. and Udell, G. F. (2006) A More Complete Conceptual Framework for SME Finance. Journal of Banking & Finance, 30, 2945-2966.

|

| [9] |

Bernanke, B. (2010). Causes of the recent financial crises. Before the financial crises inquiry commission, Washington DC.

|

| [10] |

Bernanke, B., and Blinder, A. S, (1988). “Credit, money, and aggregate demand”, American Economic Review, 78(2), pp. 435-39.

|

| [11] |

Blundell, R., and Bond, S., (1998). “Initial conditions and Moment Restrictions in Dynamic Panel Data”, Journal of Econometrics, 87, pp. 115-44.

|

| [12] |

Borio, C., Mc Cauley, R., and McGuire, P., (2011). “Global credit and domestic credit booms”, Bank for International Settlements Quarterly Review, 3, pp. 43–57.

|

| [13] |

Buccheit L. C., (2002), Sovereign Bonds and the Collective Will [article], Emory Law Journal, Vol. 51, Issue 4, pp. 1317-1364.

|

| [14] |

Bundland Commission, (1887), world commission on environment and development- WCED.

|

| [15] |

Chinn, M. D., and Ito, H., (2006). “What matters for financial development? Capital controls, institutions and interactions”, Journal of Development Economics, 81, pp. 163–92.

|

| [16] |

Chodechai, S. (2004). Determinants of bank lending in Thailand. An empirical examination for the years 1992-1996. Unpublished Thesis.

|

| [17] |

Cole, R. A. (1998). The importance of relationships to the availability of credit. Journal of Banking & Finance, 22(6), 959-977.

|

| [18] |

Cottarelli, C., Dell’Ariccia, G., and Vladkova-Hollar, I., (2003), “Early Birds, Late Risers, and Sleeping Beauties: Bank Credit Growth to the Private Sector in Central and Eastern Europe and the Balkans”, IMF Working Paper No. 03/213.

|

| [19] |

De Gregorio J. and Guidotti, E. P. (1995). Financial development and economic growth. world development vol 23, issue 3. Pp 433-448.

|

| [20] |

Djiogap, F., and Ngomsi, A. (2012). Determinants of bank long-term lending behavior in the Central African Economy and Monetary Community.

|

| [21] |

Do, Q. T., and Levchenko, A. A. (2004). Trade and financial development. World Bank Working Paper Series (3347).

|

| [22] |

Ehrmann M., Gambacorta L., Martinez P. J., Sevestre P. and Worms A. (2003), "Financial Systems and the Role of Banks in Monetary Policy Transmission in the Euro Area” In Angeloni I., Kashyap A. and Mojon B., Monetary Policy Transmission in the Euro Area, Cambridge, Cambridge University Press.

|

| [23] |

Frankel, J., and Romer, D., (1999). “Does trade cause growth?”, American Economics Review, 89 (3), pp. 379–399.

|

| [24] |

Gambacorta L, Mistrulli P. E., (2004), “Bank Capital and Lending Behaviour: Empirical Evidence for Italy”, Journal of Financial Intermediation, 13 (4): 436–457.

|

| [25] |

Halling M and Hayden, E., (2006) Bank Failure Prediction: A Two-Step Survival Time Approach, Social Economics, Business Journal of Credit Risk.

https://doi.org/10.2139/ssrn.904255

. Corpus ID: 3961090.

|

| [26] |

Huang, Y., & Temple, J. R. W. (2005). Does external trade promote financial development? CEPR discussion paper No. 515.

|

| [27] |

IMF. (2016). International Financial Statistics. Washington D. C.

|

| [28] |

Ivanovic M. (2016), Determinants of Credit Growth: The Case of Montenegro. Economics Journal of Central Banking Theory and Practice.

https://doi.org/10.1515/jcbtp-2016-0013

. Corpus ID: 55188488.

|

| [29] |

Kosak, M, Li, S, Loncarski, I and Marinc, M, (2015), ‘Quality of bank capital and bank lending behaviour during the global financial crisis’, International Review of Financial Analysis, vol. 37, pp. 163-83.

|

| [30] |

Ladime j, kumankoma E. S., and Osei K., (2013 Determinants of Bank Lending Behaviour in Ghana Jounrnal of economics and sustainable Development Vol 4, No 17 pp. 1-7.

|

| [31] |

Levine, R., (2004). Finance and Economic growth: Theory and Evidence. NBER Working Paper 10766.

|

| [32] |

Louhichi, A and Boujelbene, Y, (2017), ‘Bank capital, lending and financing behaviour of dual banking systems’, Journal of Multinational Financial Management, vol. 41, pp. 61-79.

|

| [33] |

Loutskina Z. (2012), the impact of securitization on bank’s credit risktaking behavior, Simon Fraser University.

|

| [34] |

Malede, M. (2014). Determinants of Commercial Banks’ Lending: Evidence from Ethiopian Commercial Banks. European Journal of Business and Management, ISSN, 2222-1905.

|

| [35] |

Marquez, R, Dell' Ariccia, G (2006), ‘Lending booms and lending standards’, Journal of Finance, vol. 61, no. 5, pp. 2511-46.

|

| [36] |

McKinnon, R. I. (1973). Money and Capital in Economic Development. Washington DC: Brookings Institution.

|

| [37] |

Nguyen, H. D and Dang, V. D, (2020), ‘Bank-specific determinants of loan growth in Vietnam: Evidence from the CAMELS approach’, Journal of Asian Finance, Economics and Business, vol. 7, no 9, pp. 179-89.

|

| [38] |

Okechukwu G. O. & Chukwuma A., 2008. "How Competitive and Efficient are Nigerian Ports?," Palgrave Macmillan Books, in: Paul Collier & Chukwuma C. Soludo & Catherine Pattillo (ed.), Economic Policy Options for a Prosperous Nigeria, chapter 12, pages 275-299, Palgrave Macmillan.

|

| [39] |

Olokoyo, F. O. (2011). Determinants of commercial banks’ lending behavior in Nigeria. International Journal of Financial Research, 2(2), 61.

|

| [40] |

Panagopoulos, Y., &Spiliotis, A. (1998). The determinants of commercial banks’ lending behavior: some evidence for Greece. Journal of Post Keynesian Economics, 20 (4), 649-672.

|

| [41] |

Pham, T. H, (2015), Determinants of Bank Lending, Université de Nantes working paper, pp. 1-28. hal-01158241.

|

| [42] |

Ranadi K., Hesaie J., Vosamacala S., Kabir M. N., Miah D., and Sharma P. (2021), determinants of bank lending in PICs. Griffith Asia Institute. Reserve bank of Fiji.

|

| [43] |

Sharma P. and Gounder, N. (2012) determinants of credit in small open economies: the case of six pacific island countries.: Development Economics: macroeconomic issue in developing countries’ economies Journal.

https://doi.org/10.2139/SSRN.2187772

|

| [44] |

Shaw, E. S. (1973). Financial Deepening in Economic Development. New York: Oxford University Press.

|

| [45] |

Stein J. C. (2000), “Information Production and Capital Allocation: Decentralized vs. Hierarchical Firms, NBER Working Paper No. 7705.

|

| [46] |

Takats, E., (2010). Was it credit supply? Cross-border bank lending to emerging market economies during the financial crisis. Bank for International Settlements Quarterly Review, 2, pp. 49– 56.

|

| [47] |

Tomak S., (2013). Determinants of Commercial Banks’ Lending behavior: evience from Turkey. Asian Journal of empirical research. Aasian economic and social society, vol. 3(8) pp 933-943.

|

| [48] |

Vazakidis, A. and Adamopoulos, A. (2009), “Credit Market Development and Economic Growth”, American Journal of Economics and Business Administration, 1(1), pp. 34-40.

|

Cite This Article

-

-

@article{10.11648/j.ijfbr.20241002.12,

author = {Achamoh Victalice Ngimanang},

title = {Modelling Bank Lending in Cameroon Using Two Steps Cointegration Technique

},

journal = {International Journal of Finance and Banking Research},

volume = {10},

number = {2},

pages = {32-44},

doi = {10.11648/j.ijfbr.20241002.12},

url = {https://doi.org/10.11648/j.ijfbr.20241002.12},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijfbr.20241002.12},

abstract = {This paper has as objective to model the key determinants of bank lending in Cameroon using time series data collected mainly from the World Bank database for the period spanning from 1979 to 2019. After exploring related theoretical and empirical literature, Engle and Granger two steps cointegration testing procedure was employed together with the necessary pretesting (unit root tests) and post estimation testing. Results of stationarity tests indicate that variable were a mixture of stationary and first difference. The lagged residual term possess unit root at level indicating that the variables are actually cointegarted and that ECM is relevant. The estimated cointegration regression model and the corresponding ECM were globally significant at one percent and the models were equally adequate with explanatory power of over 73 and 52 percent respectively. The results of the two models revealed that the effect of economic growth on bank lending was positive and highly significant, the effect of interest rate is negative and equally significant, then the effect of Gross Investment rate was also positive but not very significant in the short run. Based on the major findings, bank lending can be encouraged by stimulating the level of economic activities, by reducing interest rate on loans and by encouraging more investment projects.

},

year = {2024}

}

Copy

|

Copy

|

Download

Download

-

TY - JOUR

T1 - Modelling Bank Lending in Cameroon Using Two Steps Cointegration Technique

AU - Achamoh Victalice Ngimanang

Y1 - 2024/08/20

PY - 2024

N1 - https://doi.org/10.11648/j.ijfbr.20241002.12

DO - 10.11648/j.ijfbr.20241002.12

T2 - International Journal of Finance and Banking Research

JF - International Journal of Finance and Banking Research

JO - International Journal of Finance and Banking Research

SP - 32

EP - 44

PB - Science Publishing Group

SN - 2472-2278

UR - https://doi.org/10.11648/j.ijfbr.20241002.12

AB - This paper has as objective to model the key determinants of bank lending in Cameroon using time series data collected mainly from the World Bank database for the period spanning from 1979 to 2019. After exploring related theoretical and empirical literature, Engle and Granger two steps cointegration testing procedure was employed together with the necessary pretesting (unit root tests) and post estimation testing. Results of stationarity tests indicate that variable were a mixture of stationary and first difference. The lagged residual term possess unit root at level indicating that the variables are actually cointegarted and that ECM is relevant. The estimated cointegration regression model and the corresponding ECM were globally significant at one percent and the models were equally adequate with explanatory power of over 73 and 52 percent respectively. The results of the two models revealed that the effect of economic growth on bank lending was positive and highly significant, the effect of interest rate is negative and equally significant, then the effect of Gross Investment rate was also positive but not very significant in the short run. Based on the major findings, bank lending can be encouraged by stimulating the level of economic activities, by reducing interest rate on loans and by encouraging more investment projects.

VL - 10

IS - 2

ER -

Copy

|

Download